24 feb - damn son.. the old bait and switch. after all that below. i see this tweet today that instead of the trade mentioned to followers and then referenced on the show, this trade was entered TODAY

im sure some followers/viewers were surprised to see this come across. some im sure went ahead and did as recommended and sold the Mar900/950 call. not cool man. so if you did nothing..the original Feb800/850 call credit spread was exercised on you over the weekend resulting in max loss of about $36 ($3600) per lot AND if you did not follow his tweet AND just saw todays tweet and went ahead and sold the Mar800/850 call credit spread, was about $23 credit when i looked earlier ($2300 credit).. so again a $1300 loss from the roll.

now best case need stock to drop below 800 at Mar opex. im going to keep watching to see what other slight of hand surfaces.

------------------------------------------------------------------------------------------------

23feb - i don't "watch" Options Action, i listen to the podcast over the weekend and see the video clips from OptionsAction on twitter that i link to on these blogs which is why i missed this.. turns out the show did have a quick hit on this TSLA trade and the end of the segment where Tony talks his winning DPZ trade. the TSLA clip is not on twitter so i missed it and the DPZ clip ends prior to TSLA comments. but after "hearing" it today im even more pissed / disappointed. mike essentially mentioning that he tweeted the roll to the Mar 900/950 call credit spread. saying the Feb spread expired. NOTEABLY ABSENT was mentioning that the spread expired at Max Loss and that selling the Mar900/950 essentially costs you $3200 per lot. like i said below " but this advice is vague , slightly misleading, or at best- selective on the information disseminated." could really be more transparent. too bad since i like mikes well thought out trades and cool demeaner vs Nathan always being Debbie downer. the takeaway is what ive been doing the last 10years with Options Action. use the trade suggestions as an idea generator / strategy generator. for instance at the end of the SPCE clip (not included on the twitter version) Tony talks about how he has been selling Puts to finance Jan2022 long calls. that was interesting and got me looking at pricing..good idea. didn't follow but good idea regardless. don't follow the trades just because they are on air. their performance is on par with yours. its your account

-------------------------------------------------------------------------------------------------------------------

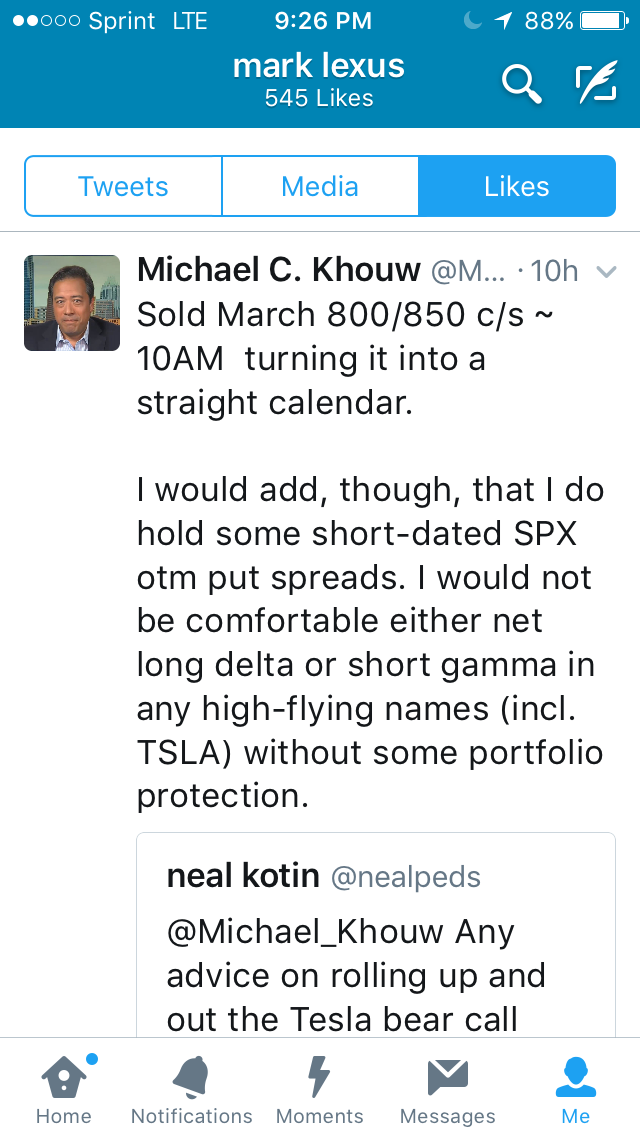

22 feb im not often surprised until this trade. start from the bottom and read the updates so far. i spotted a few people on twitter that followed along and did this trade and mike responded as such on Friday:

note the viewer is also mentioning that a roll is going to be a healthy debit. so mike is going to roll to the Mar900/950 call spread...seems simple enough but what is not being mentioned is the crazy price. has the short Feb 800/850 call spread (as in needs stock under 800 to get max profit, remember stock was 750 at trade entry).. so to roll to the Mar900/950 the Feb800/850 has to be brought back for $49ish and then the Mar900/950 call spread sold. this roll costs $32 debit ($3200)..that's nuts. stock is at 900 now so need stock to be under 900 at Mar opex to get full value of the call spread. subtract the roll $32 so really need under 868 to be breakeven on just the roll. that 868 area is about a 61% delta meaning a 61% chance that stock is ABOVE 868 at opex, so to breakeven on just the roll needs a 39% event to happen.

because the Mar900/950 call spread is not bringing in enough premium to cover the max loss of the Feb 800/850 spread is causing the huge debit

My Option #3 from below to just close out the whole thing for a $23 debit ($2300) and move on. i cant understand the logic off SPENDING EVEN MORE than this exiting amount just to keep in the trade because now you have spent $32 to roll plus the original $3+ to enter=$35. leaves you with a potential max profit of $15 on that Jun800/850.

need a series of things to happen to salvage this by Jun. first a close below 868 in Mar to get max profit from the "rolled" Mar900/950, and then assuming another credit spread somewhere for Apr / May . whats messing this up and what i didn't realize would happen is that the Jun800/850 is not gaining in value as much as i would have thought based on how high the stock went.. with the stock at 900 i would think a 800/850 call spread would be priced near full value but its only going for about $25ish now. the loss of the Feb spread far outpaced the gain of the Jun spread (which tends to happen if the stock moves way past the strikes)

a couple things come to mind when i saw this suggested roll. "risk less make more", "your first loss is your best loss", "don't throw good money after bad" . now having said all that if youre going to do this you need to think thru what to do at Mar Opex..

1. what happens if stock is above 950 (youre new Mar 900/950 gets a max loss and the Jun800/850 will gain some more).. but what do you do then

2. what happens if stock is between 850-868 (between top range of Jun spread and below breakeven of the roll/March spreads expires at max value), are you hoping for just enough gain on the Jun spread to make the whole thing a scratch?

3. what happens if stock goes back under 800 (and now your Jun spread starting losing value)

not a good position to be in. im sticking with my original gut calls on this, was not a compelling trade from the get go, better to take that first loss and exit everything and if necessary reposition yourself using better strikes vs trying to squeeze a scratch out of this one. but really disappointed in the handling of this trade by Mike and the show. we all have losers, we all try to minimize the losses, but this advice is vague , slightly misleading, or at best- selective on the information disseminated. comes with the territory of being trader on CNBC i think. has to suck to get bombarded with the "what do i do now?" "what do you recommend?" type questions but that's also part of the deal. Options Action has always been selective on what trades to cover and noticeably opts out of many losing ones. maybe for ratings. i remember years ago when i paper traded most of the trades displayed and a few of the "regulars" where consistently having losing trades (bricks). scott nations was a master brick layer. hopefully im wrong and all this works on in the right directions to at least breakevens. TSLA is turning into an Options Action widowmaker. comments / alternative trade suggestions welcome

----------------------------------------------------------------------------------------------------

19 feb - crazy that I typed this below on 9 feb …"how does it look if the stock is at 900?"... so caught a tweet from mike today responding to a viewer that followed the trade

i think im doing this right but here goes. (stock 900+ today and Feb opex Friday)

current value the Feb800/850 credit call spread $49+ debit (as in received $12.70 at sale, and would cost $49+ to close) = $36ish loss

current value the Jun 800/850 long call spread $26 (as in collect $26 if closing today, spent $16.25 to enter)= $10ish gain

net net to close the original trade i come up with a debit of $23... you spent $3.60 to put on the trade and would cost $23 more to close it.

mike is saying to roll the Feb short call spread up and out to March but not being specific about strikes..so i looked at the prices of rolling..

Roll option #1 - roll the Feb 800/850 short call spread to the Mar800/850 call spread, that costs $16+ debit to roll

Roll option #2 - roll the Feb 800/850 short call spread UP/Out to the Mar 850/900 call spread, that costs $22 debit to roll

so you see rolling closer to at the money you have to pay more. i really hope im not doing this correctly because its looking like a shitty deal if you followed along. would need stock under 800 on Mar opex to get max profit on the "rolled" call spreads

Option #3 - close the whole thing and take your lumps for $23 debit and move on to the next trade. i will try to roll as often as i need to get back to breakeven (scratch). sometimes doing a slight debit if im also selling the other side.. such has roll the Feb to Mar for the $16 debit AND if i sold a call spread for more than $16 credit.. so the call spread pays for the roll. but $16 to just roll is way out of my range. maybe take the loss and do a review of how you got into this trade and if it meet your criteria from the get go

Option #4 - depends on your conviction for this trade, your account size, and your thesis on where the stock will be on Mar opex… the only way i can see rolling to not pay is to increase the size. ive been playing with a one-lot so if you roll the Feb 800/850 to Mar 800/850 do TWO lots of the Mar800/850. essentially selling an additional Mar800/850 credit call spread.. this roll ONE Feb for TWO Mar lots shows a midpoint credit of $15 using after hours pricing. so now you would have a long Jun800/850 and (2) Mar800/850 short call spreads. tough call to make.

i really hope Options Action hits this one on Friday for an update. Mike normally doesn't have a lot of bricks.

-------------------------------------------------------------------------------------------------------------------------

15 Feb - after a week still not seeing anything compelling. granted the Feb options expires this week so hopefully OptionsAction / Mike does the viewers a solid and updates the management of this trade. when looking after hours this 4leg trade is worth $3.85 debit at midpoint. as in you paid $3.60 to put the trade on last week and to exit would have to pay another $3.85. interested to see how this turns out at Feb opex and with the secondary stock offering announcement

----------------------------------------------------------------------------------------------------------------

9Feb - Options Action show featured another trade for TSLA, have to admit I watched this clip a couple times to wrap my head around it . here is the video clip TSLA clip . even after watching a couple times im not 100% certain as to what Mike wants to happen.

Sell the Feb 800/850 call credit spread for about $12.70 credit (using after hours pricing)

and also

Buy the Jun 800/850 call debit spread for about $16.25 debit

Total debit for the 4leg trade about $3.60 midpoint (super wide bid ask)

Mikes explanation could have used more details since the show tends to be for beginners/intermediate level traders. this trade is similar to a straight up calendar spread, such as sell the Feb800 and buy the Jun 800 but with less premium.

So is mike trying to play the difference in IV between Feb(97ish) and Jun(70ish). as in selling the Feb credit spread since the premium is elevated compared to Jun, as in the Feb spread decays faster than the Jun spread turning that $3.60 debit into a credit (profit) when Feb expires... and that's the whole trade?

or is it sell the Feb spread for the elevated premium, best case it expires worthless AND THEN resell a March 800/850 call credit spread, bring in more premium. premium that is above and beyond that original $3.60 debit and ideally repeat until Jun?

or is the thesis that he is bullish on the stock thru Jun, hence the Jun call spread, and using the Feb call credit spread to help finance it. essentially spending $3.60 for the Jun 800/850

I use etrademonster and will sometimes look at the Analysis Tab and even after that im having a hard time modeling this out as to where I would make money at Feb opex and beyond. Seems to be the ideal would be stock is slightly under 800 at Feb opex, Feb spread expires worthless (you keep the full $12.70) and the Jun spread increased in value. But how does it look if, as Carter mentioned, the blowoff top from this week was the high, how does it look if stock closes at 650 at Feb Opex or how does it look if stock is at 900 at Feb opex. those are extremes I know but no one expected that price action for the last 10 days either. ThinkOrSwim or other platforms may have better modeling but im not getting a comfy feeling on this trade. seems like threading the needle a bit. that feb800 call is a 40delta still ie 40% chance stock is 800 or higher at opex. ive been operating in the 20-30 delta range with good results

would have liked to see more of an explanation as to what scenarios this will be profitable and which ones would be losers. such as max profits on this trade will be XYZ with max loss potential of 123. I will watch this one to see how it turns out and hopefully the show / twitter has an update at / near Feb opex.

I have a position in TSLA , Sold the Feb 505put at $4.20, was 5delta at the time. my thesis is to look for 25-50% of max profit wins to close out. the move in the option pricing are all based on the movement of the stock with not much IV decay. Also a straight up Put Sale if the position is threatened I can roll it out and down for credit easier than any credit spreads. I just check the pricing after hours, that put is $3.30 ish and I could roll it out 2 weeks into a March weekly and down 30+ strikes still for a credit. for my style of trading its a bit more straight forward. will watch mikes trade though, like to see how it turns out, might learn something new

No comments:

Post a Comment